Home » WHY ASIA

ASIA EXPLAINED: THE GROWTH ENGINE OF SPORTS AND ESPORTS

Asia is the growth engine of the world’s consumption, which has led to the rapid acceleration of its sports, esports and health and wellness markets. This region has the world’s fastest-growing consumer markets that offer a US$10 trillion consumption growth opportunity over the next decade (McKinsey). Growth in each key area under these sectors is a result of rising consumer optimism and overall economic prosperity across the continent. Asia is home to some of the world’s biggest economies (China ranked 2nd, Japan 3rd, India 6th and South Korea 10th in terms of GDP). Brookings states that as East Asian countries entered the global middle class, the global consumer class grew to almost 4 billion with over 50% of consumers being located in Asia. The coming decade will see an increase of a billion middle-class consumers in South Asia alone, hungry for technology innovations, education, events, media and content, thereby justifying the exceptional projected growth rates. Further, the rise of niche markets in Asia such as the “She Economy” and “Silver Economy'' is also creating new opportunities.

The significant growth in Asia’s sports, esports and wellbeing markets is being driven by increasing investment, breakthrough innovation, alongwith social and demographic change. The value chain in all these sectors is diversifying, making the current market environment extremely favourable for different players in the ecosystem. This includes leagues, teams, startups, corporates, IPs, brands and investors seeking sustainable growth and monetization opportunities.

EXPONENTIAL CONSUMPTION AND FANBASE GROWTH MOVES UP THE SPORTS VALUE CHAIN

Asia has become a crucial destination for global sporting events, and Asian home-grown professional sports leagues are gaining popularity and status on the global stage. Cricket in India offers the perfect example of Asia's massive contribution potential to the global sports ecosystem. The Indian Premier League (IPL) is now one of the highest valued sports leagues in the world, with a valuation of US$4.7 billion. The birth and funding of sports-related startups and other aspects of the sports business, in particular fantasy sports, is a result of the average Indian's deep connection to the sport.

More and more Asian sports stars making it to the global stage also helped western leagues and teams grow their influence and spark a surge of interest in different sports in Asia. South Korean Son Heung-Min, a forward for Premier League club Tottenham Hotspur and captain for the South Korea national team has been making headlines in the world of sports and generating a huge economic impact in the country.

Asia offers great opportunities for European and American sports teams and leagues to grow themselves while engaging better with Asian fans, as there is lots of untapped space in the market to be explored. Music, entertainment, art, fashion, gaming and blockchain will make great touchpoints for sports (and esports) organizations to engage with their Asian fans, especially for GenZ, millenials and female fans, which is a large population with high spending power.

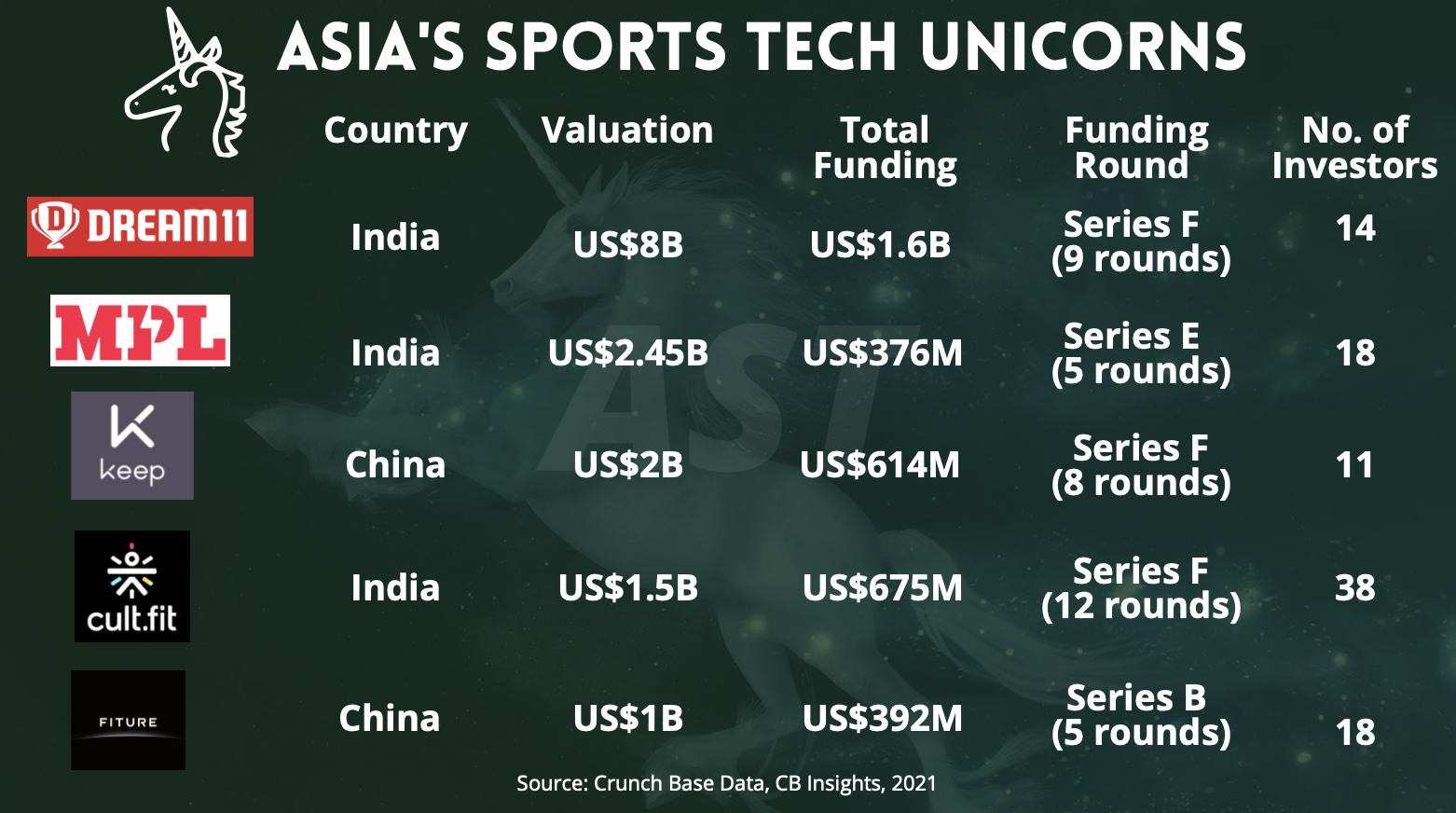

Asia is accelerating global sports tech investment and startup growth, several sports tech unicorns have emerged in Asia including Dream 11, Mobile Premier League and Cult.fit from India, and Keep and Fiture from China. The market of sports technology worldwide has been growing at an immense rate and was valued at US$11.7 billion in 2020 by Grand View Research. They projected global sports tech to grow at a CAGR of 16.8% from 2021 to 2028, with APAC expected to be the fastest-growing regional market during this period. By 2025, Asia-Pacific itself is projected to reach US$10.8 billion in value, which is equal to the market’s global value in 2021.

APAC also leads growth in the global sports equipment and apparel market. A recent study by Allied Market Research projects that the global sports equipment and apparel market will hit US$930.5 billion by 2031, with APAC poised to grow at a CAGR of 10%, which is the fastest-growing region. Driven by the resumption of events, an increase in the popularity of fitness activities, and the growing adoption of sports technologies, Asia’s market growth has returned to pre-pandemic levels. Besides consumption, Asia also has a high share of sporting goods production and export.

ASIA'S DOMINATION IN ESPORTS AND OPPORTUNITIES

Asia is an esports powerhouse, its continued growth is led by an expanding user base, game publishers and government support for the industry in many countries. China leads all markets with revenues in the esports industry increasing 25% year on year in 2019, raking in $17.4 billion from PC client esports games, mobile esports games, as well as offline events, esports live streaming and sponsorship. The market reached US$20.8 billion in 2020 and US$24.5 billion in 2021 with growth spurred by esports tournaments and live streaming. South Korea is known as the “mecca of esports”, with the country being home to many of the world's most successful and valuable players and teams. Two Asian teams, Korean teams Gen.G and T1, made the Forbes World’s Top 10 most valuable esports organizations list in 2021. They ranked 8th and 10th with valuations of US$250 million and US$220 million respectively.

Asia features a large youthful population that is mobile connected through 4G and 5G adoption continent-wide. As a result, mobile esports has exploded in popularity with Esports Insider explaining that “mobile esports is a phenomenon across Southeast Asia (SEA)”. Mobile titles like Arena of Valor, PUBG Mobile and Mobile Legends: Bang Bang (MLBB) have amassed viewership figures above 1 million peak viewers across multiple events in SEA due to large fan bases in the region. The 2022 MLBB SEA cup in Malaysia attracted a peak viewership of 2.8 million fans.

The Philippines particularly stands out as a key esports and gaming market in Asia with tremendous growth potential. Driven by mobile gaming, the market features over 43 million active gamers with a 12.9% year-on-year growth rate since 2017 according to YCPS Marketing and Communications Group. Statista has indicated that revenue from mobile gaming will jump from US$1 billion in 2021 to US$1.5 billion by 2025. There is also growth potential for traditional esports, driven by local gaming-focused media and entertainment companies like Tier One, the market features a lot of untapped potential.

Asia also offers immense opportunities for Web3-related businesses, such as gamefi or play-to-earn platforms to take off. CoinDesk highlights that many adults in SEA are bypassing traditional banking and adopting Web3 applications. The Philippines and Vietnam rank first and third respectively among the top 15 countries that most actively use MetaMask. Gamefi, or play-to-earn is extremely popular in the region as a result, with play-to-earn opportunities allowing many to supplement their current incomes. Vietnamese blockchain game Axie Infinity currently has nearly 9 million players, with much of the user base being located in SEA.

FITNESS AND WELLNESS IS NOW A BIG BUSINESS IN ASIA

Triggered by the pandemic, the demand for digital fitness and wellbeing solutions among Asian consumers will only continue to increase. Asia’s recreational physical activity market is led by China, with a market valued at US$109.3 Billion and second globally only to the USA. However four of the top ten, and six of the top twenty largest markets worldwide hail from Asia-Pacific, according to Global Wellness Institute. Notably, Japan is third worldwide with a US$43.9 billion market. Even relatively small regions like Singapore and Hong Kong’s recreational physical activity markets perform admirably on the world stage.

The top six Asian markets are highly mature and developed physical activity markets, primarily due to the more intense competition between more established players. Their growth is also a result of the active participation of their governments, which promote physical activity through public education programs. Some examples are South Korea’s Program 7330 and Singapore’s Active Health program. China itself has been experiencing explosive growth because of its government’s support through sports policies, the proliferation of gyms and fitness studios in its Tier 1 cities, and the widespread adoption of fitness apps and online platforms.

Since 2017, Asia has been leading the digital fitness and wellbeing device market (Statista, 2022), and it will continue to explode exponentially. As technology related to fitness and wellness is in high demand in Asia, there will be more and more innovators offering diverse and accessible digital solutions for Asian consumers. As mentioned previously, digital coaching and wearable technology are becoming ever more popular due to more affordable, yet more reliable products for data collection and management, alongwith rising athlete adoption. This is especially true as the industry transitions to a more data-driven sports culture with fitness tracking improving casual fitness activities, training and even in-game decisions.

WHAT'S AHEAD IN ASIA'S MARKET?

The Asia market provides an exciting frontier in the world of sports and can be looked at as the engine of growth for this industry. The region is perfectly poised for growth across all verticals under the greater sports ecosystem from traditional sports to esports, fitness, health and wellness. Opportunities are available beyond China and India, into the varied and complex Northeast Asia, Southeast Asia and Oceania region, each offering its own unique competitive advantage. Growth and profitability in Asia’s sports ecosystem are driven by three components - innovation, consumption and investments. With both macro and micro factors moving up the sports value chain, increasing capital inflow and more players entering the market, the opportunities of Asia's sports ecosystem cannot be ignored.

AST is ideally placed to help you gain the exposure to Asia that you need. Our team is ideally set up to provide Financial Advisory, Asia Market Entry and Growth Strategies, apart from a host of complementary services.

To get an in-depth understanding of the services we provide. Our experienced teams based in Hong Kong, Singapore and Taiwan use their unique insights and connections to help you grow and scale:

Request a free consultation for a better understanding of the business and investment opportunities offered by the Asia Market.

LET'S CONNECT